Control Theory Without Controls1Abstract

We draw on the insights of Wynne Godley & Francis Cripps (1983) and Martin Shubik (2004, 2012). The former provided a purely structural account of macroeconomics with no microfoundations. The latter offered a constructive critique of general equilibrium theory for the purpose of developing a theory of money and financial institutions. We join the two perspectives within the ambit of General Systems Theory (GST). Accordingly, we formulate and test for the stability of models of the capitalist system first (Godley & Cripps). Then, we compare and contrast General Equilibrium and ‘Nash Equilibrium’ solutions of the same capitalist economy (Shubik). The GST postulate connecting the two is that control variables or strategies are immanent or diffused within the system. We provide conditions under which the economy can be stable under debt-induced expenditure and conditions under which finance can be destabilising. Keywords: structure and functioning; reduced form of a game JEL: B52; E12 1 The comments of two anonymous referees were instrumental in correcting errors and adding precision and focus to an earlier draft. I am entirely responsible for the final product.

Introduction

An open door to entry into off-mainstream accounts of the economic process is the role played by money in the system. The stories told in general equilibrium economics as well as the theoretical agenda professed there is entirely theory-driven, appealing to the model-building skills of its practitioners. No correspondence with empirical reality is sought. In contrast, the framework of Wynne Godley and Francis Cripps, 1983, (G&C, hereafter) grew out of their engagement with a Cambridge macroeconomic policy model of their time. Consequently, their system of definitions and equations consists of variables which are measurable. In fact, their framework is an offshoot of the development of National Income accounting, staying close to Keynes’ orientation towards the study of the economy as a whole. They gave a twist to their representations reflecting their Keynesian persuasion in contrast to emphases laid on other relationships in standard models. All entries in their accounts are monetary and the connections between households and firms on the one hand and the Central Bank and the Treasury with commercial banks in between are made. Care is taken to distinguish between stocks and flows (changes in stocks). The distinction naturally leads to handling the current values of variables and one-period (at least) lagged values of the variables. Their array of identities and definitions are richer than most and we mix and match them. Difference equation systems emerge and the coefficients are “stock-flow norms”, an innovative contribution to the subject by G&C. These are steady-state ratios between variables that are empirically robust. The importance of some might decline with time and new norms can emerge as the economy evolves. Different configurations throw up different pairs of agents and it is sufficient, though not necessary, to solve for their objectives, subject to the constraints posed by the economy. Martin Shubik’s class of models was not far behind in spelling out the institutional constraints under which people operated. However, he made their maximands explicit and solved for their optimal plans. All through, he was concerned with the different mechanisms by means of which societies dealt with monetary phenomena like “not enough cash”. He studied defaults and punishments but was inspired by their role as empirical social sanctions. Our task then is to preserve the structural sanctity of the capitalist economy and, at the same time, scrutinise the plans of consumers and producers as they maximise their payoffs subject to the rules and regulations imposed by the economy. The feedback operation must not be missed. The dynamical system under which workers and firms operate is generated by them by means of their actions. In turn, the structure determines their functioning. We have enunciated the underlying principle of Systems Theory. We will examine cases where the identity of agents does not matter when solving out for the stability of social systems. In the typology of the great systems theorist and planner, János Kornai, systems theory goes hand-in-glove with the concept of control of material processes (Vahabi, 2017). The sequence of questions to be asked are: what is the ensemble of decision-making of subsystems required to secure social ends; what is the information required to feed the decisions to those ends and, finally, what are the appropriate motivations in the form of codes of conduct that must be installed. In the jargon of GST, supremal units and infimal units substitute for the planner and agents. Modern complex systems theory is more self-conscious about the use of the category subsystems instead of groups of people (Davis, 2018). The interaction between subsystems influences their choices as well as determines the contours of the overall system of which they are constituents. A final venerable tradition we need to recall is old Austrian economics. Especially with the scholarship of von Hayek, the economy was viewed as a “spontaneous order” emerging out of the choices made by myriad agents as they operated with local information sets. No individuals or coalitions are in command. The economy is a negative feedback system. State-level information feeds back in a learning process. A word on the formal language that follows. Mathematics in economics evokes the Bourbaki strategy of axiom-theorem-proof. Two practices ensue. The mathematicians relax the axioms and/or generalise the theorems. The economists incorporate features of the world through extending the set of axioms. The system is closed. In contrast, in the open systems strategy deployed here, categories are carved out of economy-wide data. The quantities are connected by arithmetic. They are identities. The dynamics in the relations might be more or less explicit or, as in our case, teased out of the material. The context is past and present and, in the case of government policy appearing in self-evident fashion, the future. The idea of ‘emergence’ is invoked to signify that the conglomeration of individual actions alone is insufficient to explain large-scale economic outcomes (Tubaro, 2009). Emergence connotes novelty, the appearance of something new, mysteriously fashioned out of existing data. The new phenomena cohere and are always generated in a context. The notion of ‘institutional emergence’ is connected (Elsner, 2015). Emergence has three key properties: supervenience, irreducibility, and downward causation (Festré, 2015, 2018). The drivers are self-organisation and non-intentionality. People operate by means of rules which are units of knowledge and thus the building blocks of wealth. Knowledge is tacit and is exemplified in focal points which are solutions of coordination problems. The reasoning is induction and not deduction. Identities become equations through the introduction of institutions. Different sets of equations are explored. The benefit in political economy is the emergence of classes (Lawson, 2015). Some sensitive observers today are deeply concerned about the evaporation of the productive classes and their replacement by a unified parasitic financial class. We will examine the implications of the introduction of a rentier class that anticipates revenues earned as capital gains. The motive is speculation as rents are earned on the purchase and sale of shares and bonds and, recently, share buybacks (Michie, 2020). No attention is paid to bank borrowing and production. Invoking the concepts of Marx, we deal with classes an sich below and not “class-for-itself action”. Secondly, in mainstream macroeconomics, market-clearing is a basic result. Studies in the existence and stability of general equilibrium are conducted with reference to this point. In contrast, notably with the orientation of Hyman Minsky, the capitalist economy is captured at any point of time in the form of interrelated balance sheets. All elements are continuously being perturbed. Scholars like Dani Rodrik speak of two or three balance sheets in an economy currently being out of sync without appreciating that all balance sheets in an economy are connected. It was left to stock-flow-consistent (sfc) macroeconomics to use the discipline of double-entry booking in a macroeconomic ledger to demonstrate that all the items had to sum to zero. A positive item cancelled out with the identical item with a negative sign. Stability or instability had to be proved with reference to real-monetary-financial connections. The next section provides a sfc account of the macroeconomic process. We derive a two-by-two difference equation system by manipulating identities and definitions. The stability condition is spelled out. The state vector suggests two classes. In the following section we proceed to solve out for the dynamic optimisation problems of the two classes constrained by the difference equations of the earlier section. Both General Equilibrium and ‘Nash Equilibrium’ solutions are worked out. The discrete charm of Godley and Cripps We work with the sfc framework of G&C, 1983. The classic remains unparalleled in its lucidity and depth despite the profusion of work it gave birth to. One illustration of a constructive development is the connection with a Steindl-Minsky model that has recently been made (Gallo & Pereira Serra, 2020). The contribution to the Post Keynesian literature is the attention given to initial conditions in terms of the level of existing debt and inventories. The notational conventional followed for change, taking inventories, I, as an illustration is ∆I ≡ I – I-1 where I denotes inventories at the beginning of the current period and I-1 stands for the stock of inventories at the end of the previous period. Denoting final sales, FE, as a combination of private sector purchases, PE, and government expenditure, G, FE ≡ G + PE, our first macroeconomic identity follows (G&C, 1983, p. 33, p. 102).

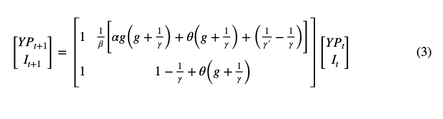

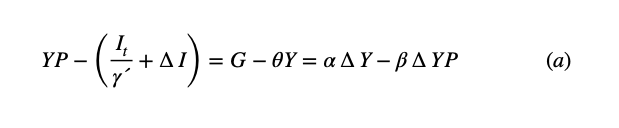

If inventories are financed by credit lines with banks, the total value of inventories in the economy will be equal to the debt of the production and distribution sector to banks (G&C, 1983, p. 73). Our first sfc norm is given by the steady-state money/income norm alpha. Denoting by FA the stock of money in the steady state, we have FA = αY. Government borrowing from banks is GD. Net government income is YG where YG = θY, and Y is national income with θ as the tax rate. We are in a position to offer the first fundamental theorem of macroeconomics: the private sector surplus (the left-hand side of the next equation) equals the government deficit (the right-hand side of the equation) (G&C, 1983, pp. 105-106). Noting that disposable income YP = (1 - θ)Y and denoting private sector debt by PD, we get the following important expression (G&C, 1983, pp. 105-106). End-period private debt PD (G&C, 1983, p. 149) is believed to be connected with disposable income by a debt/income norm, beta. That is, PD = βYP. We denote the proportionate change in the value of inventories in each period by g (∆I = gI) (G&C, 1983, p. 95). The ratio of opening inventories, I-1, to sales, FE, is γ and, in the case of the restriction of final expenditure to private expenditure, PE = I-1/γ′. (The latter is our own contribution, illustrating the constructive possibility of sfc norms.) Expressing equations 1 and 2 in difference equation form and reverting to a more familiar notation for time, we have the following dynamical system which is derived in an Appendix.

The stability condition suggests the following. The fiscal deficit is at the heart of equation 2 but its components break up in the requirement. Now or never is government expenditure consisting both of FE reflected in γ, and PE reflected in γ´, at the root of resuscitation schemes for economies the world over. The sophistication of G&C extended to introducing money in the first few pages of their book without, even subsequently, referring to central banks or commercial banks in any detail. In our stability condition the money-income norm cancels out. Our mandate, however, compels an institutional fleshing out. Indeed, the elaboration is urgent as theorists and practitioners forecast the eventual demise of commercial banking. With that, credit disbursement in the form of idiosyncratic relationships between banks and entrepreneurs will fade away. It is natural, therefore, that some economists have even advocated a return to an elaborate form of nationalised banking. The institutional impetus is provided by the public deposit banks (PDBs) of the early 1600s which stopped the hyperinflation during the thirty years war (1618-1648) in its tracks (Schnabel & Shin, 2018). PDBs were similar to modern central banks insofar as their deposits were a platform for a cashless payment system. Transactions between account holders would be settled from one account to another or through bills of exchange. The proviso that all bills of exchange in excess of a figure had to be paid at the bank compelled merchants to open bank accounts.

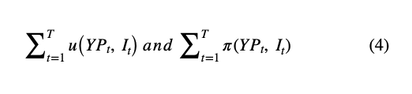

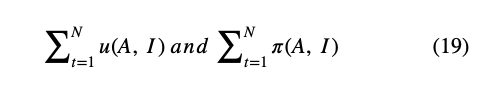

The economy is not touched by finance yet and we can assume that Main Street, representing production on the one hand, and Wall Street do not cross. The structural backdrop to averting financial crises is the principle of the Chinese Wall shielding commercial banking from investment banking canonically embodied in the Glass-Steagall Act of 1933 in America (Tarullo, 2019). The resulting stability in borrowing and lending for producing and consuming goods and services called for no more than light-touch regulation for forty years. The Dodd-Frank Wall Street Reforms and Consumer Protection Act of 2010, while focusing on systemic risk, forewent the structural separation principle of the 1930s. “Mathematical Institutional Economics” The title of this section was coined by Shubik to propose a research agenda for the development of a rigorous political economy that was theoretical but not abstract. He critiqued neoclassical economics for removing itself from the reality of monetary and financial arrangements. Accordingly, his general equilibrium economics, while skeptical of the Walrasian strain, embraced Edgeworth. Thus, Shubik developed a vocabulary for the thrusts and parries of one agent and then the other as they moved from one corner or the other in the box made famous by Edgeworth. Different conditions will determine different equilibria, a result echoed by the ‘varieties of capitalism’ approach to political economy that incorporates rational choice theory in the strategic interaction between agents. However, their ‘play’ is filtered through institutions. Indeed, we will demonstrate that it is a matrix of dos and don’ts that determine behaviour and outcomes (Stockhammer & Ali, 2018). We observe that two classes emerge naturally by the formulation. They are consumers (YP) and entrepreneurs (I). These agents will maximise their following utility and profit functions respectively subject to the constraint given by equation 3. We deploy the definition of dynamic games that treats the subject as a multi-agent control problem. Observe that a ‘reduced form’ representation of the game emerges naturally. There are no strategies, only components of the state vector, income/wealth in the form of stocks/flows in the payoff functions. The state vector is given by (YP, I).

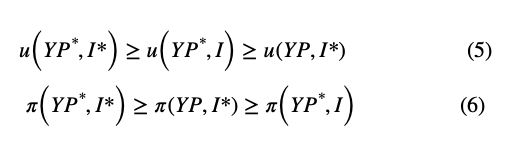

We will substitute for the expression ‘general equilibrium’ to avoid confusion between the common connotation of the term and Shubik’s special treatment. Our definition of a macroeconomic equilibrium (ME) is a vector (YP*, I*) such that the following inequalities hold.

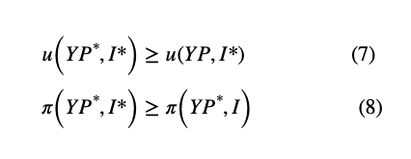

In contrast, the ‘Nash equilibrium’ (‘NE’) (italics because there are no strategies) is implied in the next expressions.

In the case of the first definition, we provide a different representation of the spillovers that define general equilibrium. Usually, they are externalities, positive or negative, between markets. In our case, the elements of the state vector not determined by an agent must influence her payoffs. In the case of the ‘Nash equilibrium’, on the other hand, each agent is only interested in a portion of the state vector assuming the level of the other portion of concern to the other agent. Market clearing is not part of either definition. Secondly, shocks to technology and preferences will not figure below. We distance ourselves from the Real Business Cycle literature in these senses (Gali, 2018). The extensions of those models continue to be fixated on equilibrium which are now stationary fluctuations caused by exogenous shocks. Frictions of different kinds are introduced so as to amplify the effects of the shocks. These New Keynesian assumptions are artificial and are no more than speed bumps on the road to equilibrium. Not subscribing to the research practice, we are able to capture the implications of asset price inflation. The potential instability that arises is endogenous. The economy is in disequilibrium in the short run (Renault, 2018). The stickiness of prices assumed by the French neo Keynesians, in contrast, is empirically evocative. Thus, real wages do not vary with unemployment, labour supply is unresponsive to the real wage. The prices of manufactured goods are insensitive to demand conditions. The economy is captured by queues, lengthening delivery dates, spillovers into substitute goods. Capacity is underutilised and producers accumulate inventories.

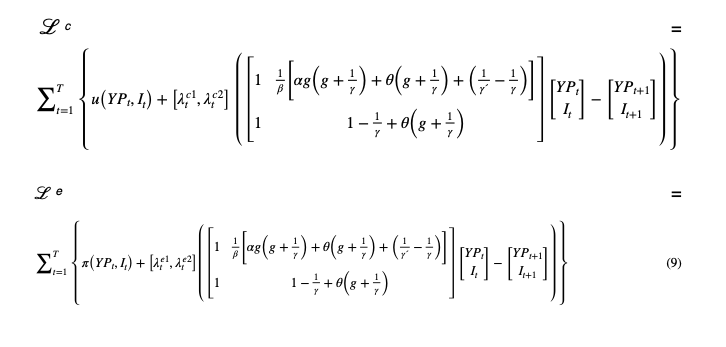

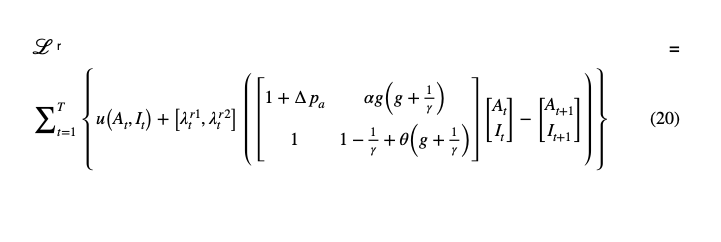

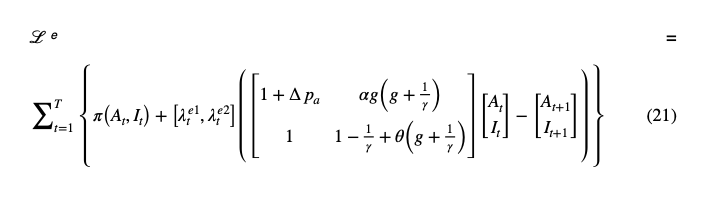

We proceed to calculate the ME and the ‘NE’ in the case of two regimes, in turn. Real stability The macroeconomic equilibrium We distinguish the consumer and the entrepreneur by the superscripts c and e respectively and the shadow prices of the stocks in the current period is the familiar vector λ, superscripted to distinguish the two constraints summarised in equation 3. The Lagrangians for the problem are as follows.

The first order conditions for the state variables are given next.

Taking the derivatives with respect to the shadow prices we get the system equation 3, now to be solved out simultaneously with the above first-order conditions to derive the optimal values of the components of the state vector.

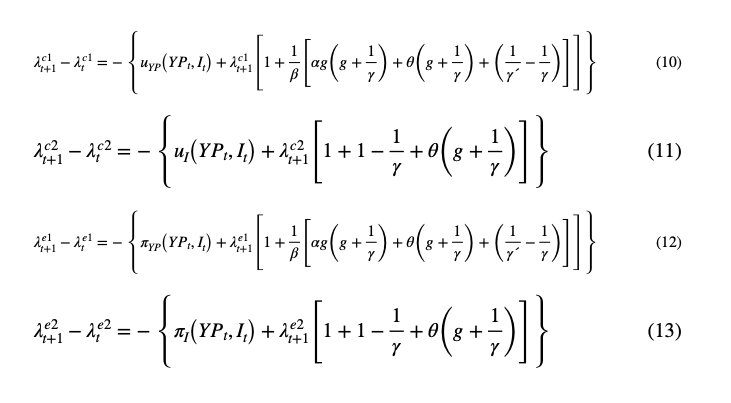

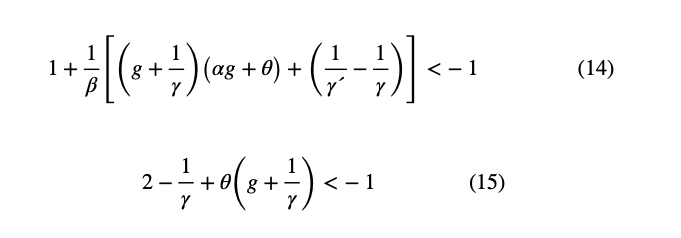

Each of the four equations above are linear and independent. The equilibria of the equations emerge naturally by recalling an optimality condition when solving out for the static problem of a representative agent. The marginal utility and profits with respect to the respective arguments must equal the shadow price of the respective constraints on the right-hand side. The left-hand side, then, will be zero. The equilibrium is a sink if the following conditions hold. All solutions converge to the equilibrium point. If the inequality is reversed, the equilibrium solution is a source. All solutions diverge from the equilibrium point.

Other things being equal, our equilibrium is a source. It is a sink if the value of γ is appropriately ‘high’. Our earlier remarks about government expenditure are endorsed. We recognise the government as a built-in or automatic stabiliser. The perspective is a refreshing antidote to the new classical precept that a ‘high’ level of government expenditure is destabilising.

The ‘Nash equilibrium’ In the case of the ‘NE’, each player optimises the value of the component of the state vector of own interest, holding the value of the other component of the state vector of interest to the opponent at the optimal level. Thus, the conditions now are as follows.

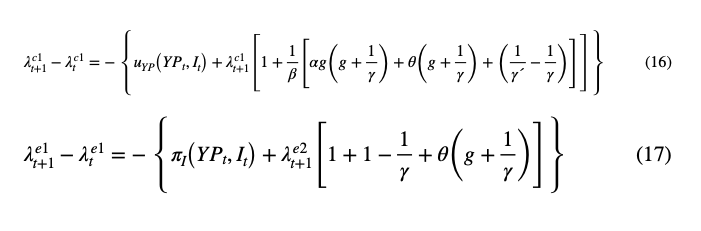

The earlier remarks carry over. Only, the number of constraints and multipliers are reduced and the marginal conditions for each agent vis-à-vis all elements of the state vector do not have to be computed. Clearly, while a general equilibrium is a Nash equilibrium, the opposite is not necessarily true.

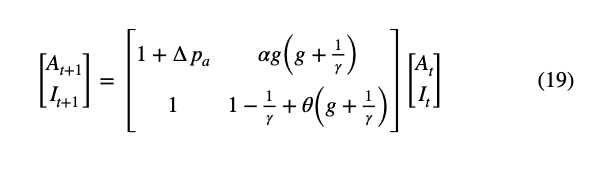

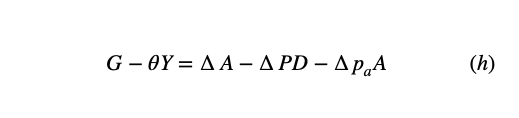

Financial stability Another flow identity introduced concerns the stock of financial assets, A. With this step, we need to introduce capital gains and losses in a revaluation term, RVA. The macroeconomic equation is ∆A = ∆GD + ∆PD + RVA (G&C, 1983, p. 274). We provide the following expression of the capital gains term RVA, Δpa.A, where A is the stock of financial assets and pa the price. Our master equation 2 translates to following expression.

The system reduces to the following matrix equation derived in the Appendix.

The money/credit process is explicit this time in our terse stability condition. Tied to the money-income norm is the tax rate as a stabilising device. This stipulation is original given the various other reasons for ‘high’ income taxes. Secondly, the condition for stability underscores the well-known notion that the ‘search for yield’ is destabilising. The consequence is the Minsky prognosis that financial boom and bust cycles will recur with newer financial innovations and with capital gains following capital losses (Kregel, 2018). Stability is ensured by productivity gains validating debt. When, instead, capital gains substitute for productivity, instability is endogenised.

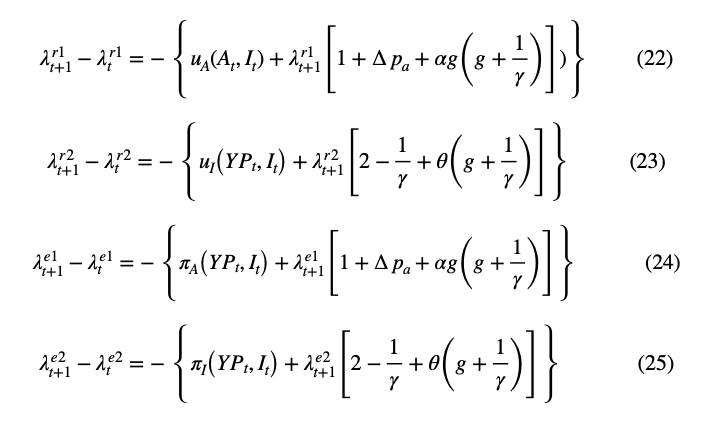

We call the new character that owns and accumulates wealth the rentier. The term is functional and does not exclude the wage income which a household might earn. Now, the rentier, distinguished by the superscript e, and the entrepreneur will maximise their utility functions below subject to the dynamical system given by equation 18.

The Lagrangians this time are

The macroeconomic equilibrium

Once again, the first order conditions for the ME are the following. The first order conditions for the state variables are:

All our remarks made earlier carry over.

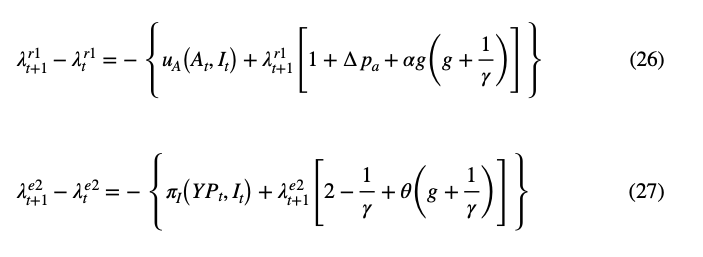

The ‘Nash equilibrium’ Following in our earlier footsteps, the optimization conditions for the ‘NE’ are:

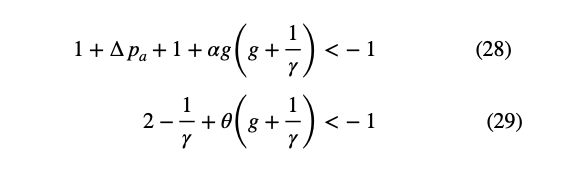

The discussion surrounding equilibrium solutions above is identical. Once more, the equilibrium is a sink if the following conditions hold. The equilibrium is a source if the inequalities are reversed.

The requirement for a sink can be met with a massive collapse in asset values. A case for bursting bubbles in the form of ‘high’ and rising capital gains is made. In addition, as earlier, large-scale government expenditure would be the backstop. Other things being equal, however, the equilibrium is a source. So-called ‘core meltdown risks’ underpin securities markets in the US where, in both a relative and in an absolute sense, the provision of credit relies heavily on capital markets in contrast to bank lending. The modern route to bubbles and crashes, especially in the US, has been charted as follows (Duffie, 2019). Financial intermediation in US capital markets depends on large dealers who make markets by buying securities from investors who are potential sellers and selling them to investors who are potential buyers. The meltdown of 2008 was displayed in the innovation of the repo, a repurchase agreement which is a short-term debt. Before the crisis, Goldman Sachs, Morgan Stanley, Lehman, Bear Stearns, Merrill Lynch, secured hundreds of billions of dollars in overnight credit in the repo market. On each repo, a dealer transfers securities as collateral to its creditors in exchange for cash. When a repo matures the next morning, the collateral is returned to the dealer and the dealer must return the cash with interest. Market participants often held the securities provided to them by dealers in accounts with two “tri-party” agent banks, JP Morgan Chase and Bank of New York Mellon. In like manner, repo investors transferred their cash to the deposit accounts of the dealers at the same two banks. When the dealers’ repos matured each morning and they repaid the cash investors, the dealers required intra-day financing to support their inventories of securities until fresh repos could be transacted at the end of the same day. This intra-day credit was provided by the aforementioned agent banks.

If a major dealer could not roll over its secured funding on a given day, a tri-party bank’s balance sheet would become unbalanced by the risk of revaluations of hundreds of billions of dollars’ worth of securities provided by that dealer as collateral. In that case, the tri-party bank would have an incentive to dump the collateral securities. A fire sale would be contagious causing a dramatic drop in the prices of weaker collateral. In sum, nonbanks were instrumental sources of credit for the real sector in the years preceding the last crisis. Their growth went along with an increase in debt financing. Short-term borrowing cumulated on the unfounded belief that it could be continuously rolled over. Can we devise norms to ameliorate these buildups and breakdowns? A norm that has been proposed to stabilise household debt is a loan-to-income ratio (Aikman et al, 2019). Discussion

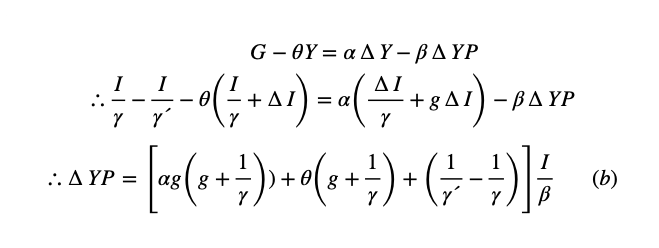

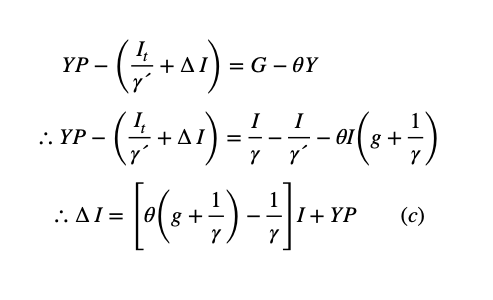

Modern sfc economics goes back to the work of Morris Copeland in the 1940s and 50s with his flow of funds matrices (Focardi, 2018). The questions that double-entry bookkeeping could answer included the following: When the total purchases of aggregate output go up, how does the stock of money increase? In a dynamic extension, what part does debt play in the cyclical trajectory of money flows? Later, scholars like Charles Goodhart developed the flow-of-funds equation wherein neither the private sector nor the government were accorded pride of place. Indeed, in the equation associated with Goodhart, the Public Sector Borrowing Requirement (PSBR) alone moves to the left-hand side, all the other elements to the right-hand side. The contemporary refinements of sfc economics include the incorporation of purchasing power in the definition of money, thereby holding fast to the empirical orientation of the model. When even labour is exchanged for money, a credit for purchasing commodities is acquired. Money requires an existing structure of ownership of goods supported by institutions. Money does not create ownership but facilitates the transfer of ownership. Secondly, analysis is conducted at the level of “subsystems” rather than individuals so as to continue to avoid committing the fallacy of composition that Keynes warned against. The particular example provided here is that high corporate profits and supernormal profits in financial markets should have resulted in an increased demand for goods and services and inflation, post crisis. However, the absence of that result is due to the development of an asset bubble concurrent with money generation. Another great scholar who melded institutional economics and game theory is Masahiko Aoki. History is salient here as is the focus on equilibria and the relative unimportance of players. The long-term experiences of members of a society are self-sustaining. In developments of his framework, agents are assumed to work with parsimonious models of the economic process in comprehending portions of the state vector (Mannara & Sacconi, 2019). Each agents is aware that other agents are, equally, cognising different elements of the evolving state of the world. Yet, Comparative Political Economy (CPE) of which he could be regarded as a co-founder has been found wanting on the ground of not incorporating financial bubbles and crashes in its repertoire of ideas (Schwartz & Tranoy, 2019). The reason advanced is the capitulation of the macro of the research agenda to the unwithstandable pull of micro, from the political economy of effective demand failures to the economics of supply-side economics. Thus, the common coin of concepts is ‘governance’ and ‘optimal institutional forms’. A crossing in our two roads is the anthropological definition of ‘social structure’ (Ballet, 2018). A social structure is a system of stable relationships between people based on steady-state norms. Also, in the absorption of empirical evidence and the collection of handheld and novel sources of historical data, our research strategy is not antithetical to “enculturation” which is a focus on the group rather than the individual (Mayhew, 2018). The ensemble of institutions people are born into are path dependent but also contingent. People can change them. After all, the future is subject to incalculable uncertainties propelling people to ‘create paths’. Kaldor, along with Marx and Veblen, were especially eloquent on the creative functions of markets in this regard (Finch & McMaster, 2018; MacKinnon et al, 2018). Locked-in paths can be broken by “mindful deviation” by knowledgeable actors. The new roads must be routes through capital accumulation involving, in turn, processes of production, circulation, and consumption. To that end, “social purpose” might have to be specified (Baker, 2018). For instance, the services of alternative banking arrangements that are more stable can be sought (Karl, 2015). A variety of different models support a dual bottom line, individual profit and aggregate benefit. Interest rates are of less importance and the real economy is the focus of attention. Structured financial products and proprietary trading are eschewed. Inevitably they are specialist institutions steeped in nuanced information about their clients which enables them to make informed assessments of risk. Their credit monitoring skills are superior and they are proactive with advice particularly to new and inexperienced SMEs. From the other end of the transaction, people prefer alternative banks. The reputation risk is lower. Since their liability base is small depositors and they are mostly independent of the interbank market they are protected from contagion. Conclusion In the first few pages of their foundational classic, G&C introduce debt financing by households and governments. The identity in which it is embedded is linked with other fine-grained identities all connected by stock-flow norms that ensure that the economy is a coherent system. The assumption that borrowing as a precondition to generate income goes back to the classics with the concept of the wage fund as a given prior. It is a small but important step to postulate that a bank must be in attendance to advance the wage bill, and the wage fund becomes the money wage fund instead of a fund defined in terms of corn. Post Keynesians introduced behaviour later in the form of consumption functions driven by social practices. The search for a ‘truer’ investment function continues. Shubik preferred to operate with ‘first principles’. The appeal of that choice could be made on the basis of an alternative way our study could have proceeded. Michał Kalecki developed a model taking off from the less-familiar way of breaking up National Income, into Wages and Profits. Behind these categories are workers and capitalists, respectively, and it would not be unnatural to model the interaction between them as an antagonistic or a cooperative game played between the two classes. The appeal of G&C macro is that the words ‘real’ and ‘nominal’ are not used. Finance enters without fanfare. Workers and capitalists can be rentiers instead of producing goods and services. They maximise their payoffs defined on their information sets, and their choices at the same time determine the level of state information. We offer a general context to consider the stability requirements of ‘real’ and ‘financial’ regimes. Appendix We use equations 1 and 2 and the sfc norms introduced to derive equation 3. Rewriting equation 2 using the relevant sfc norms,

The equation can be considered in its two parts and a dynamical system in YP and I reveals itself. (Y is national income subsuming all).

Thus, first,

Second,

We employ the more familiar notations to write difference equations, ∆YP ≡ YPt+1 – YPt and ∆I ≡ It+1 – It to write equations b and c in the state-space representation of equation 1.

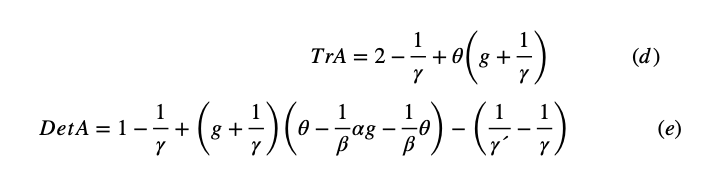

We proceed in familiar fashion to investigate the stability of the model. For the purpose, the Trace and Determinant of the coefficient matrix, call it A, must be calculated. Thus,

The zero solution of the difference equation is said to be asymptotically stable if the following condition is satisfied (Zhang, 2006, p 269).

In our terms this condition is expressed as

Recalling that all the coefficients are proportions, numbers less than unity, the condition will be met with robust values of the coefficients in the denominator of the expression.

We now derive equation 6. For the purpose, we rewrite the appropriate portion of 5. Recalling that all the coefficients are proportions, numbers less than unity, the condition will be met with robust values of the coefficients in the denominator of the expression. We now derive equation 6. For the purpose, we rewrite the appropriate portion of 5.

We also recall that ∆FA = ∆GD + ∆PD. Substituting into the equation above,

Combining c and i in matrix form, we get equation 6.

Our stability condition now translates to

The complication here is that ∆pa can take a positive value (a capital gain) or negative value (a capital loss). In both events, we find that only the value ∆pa = 0 meets our stability condition (under weak inequalities) and with θ > αg.

References Aikman, D. Bridges, J. Kashyap, A. and Siegert, C. 2019. Would Macroprudential Regulation Have Prevented the Last Crisis? Journal of Economic Perspectives, 33 (1), pp. 107-130. Baker, A. 2018. Macroprudential regimes and the politics of social purpose, Review of International Political Economy, 25 (3), pp. 293-316. Ballet, J., Anthropology and Economics: The Argument for a Microeconomic Anthropology. Cahiers du GREThA n0 2018-14, Bordeaux, France. Davis, J. B. 2018. Ethics and Economics: A complex systems approach. Department of Economics, College of Business Administration, Marquette University, Working Paper No. 2018-01, Wisconsin, USA. Duffie, D. 2019. Prone to Fail: The Pre-Crisis Financial System. Journal of Economic Perspectives, 33 (1), pp. 81-106. Elsner, W. 2015. Policy Implications of Economic Complexity and Complexity Economics. MPRA Paper No. 63252 posted 28 March 2015. Festré, Agnès, 2015. Michael Polanyi’s economics: a strange rapprochement. GREDEG Working Paper No. 2015-36, France. ___________, 2018. Hayek on expectations: The interplay between two complex systems. GREDEG Working Paper No. 2018-28, France. Finch, J. H. and McMaster, R. 2018. History matters: on the mystifying appeal of Bowles and Gintis Cambridge Journal of Economics, 42 (2), pp. 285-308. Focardi, S. M. 2018. Money. London & New York: Routledge. Gallo, E. and Pereira Serra, G. 2020. Inventories, Debt Financing and Investment Decisions: A Bayesian Analysis for the US Economy. Department of Economics, New School of Economic Research, Working Paper No. 05/2020, New York. Gali, J. 2018. The State of New Keynesian Economics: A Partial Assessment. NBER Working Paper No. 24845, National Bureau of Economic Research, Cambridge, MA. Godley, W. and Cripps, F. 1983. Macroeconomics. Oxford: Oxford University Press. Karl, M. (2015). Are ethical and social banks less risky? Evidence from a new dataset. WWW(Welfare Wealth Work)FOREUROPE Working Paper No. 96, Vienna, Austria. Kregel, J. 2018. Preventing the Last Crisis: Minsky’s forgotten lessons ten years after Lehmann. Levy Economics Institute of Bard College Policy Note No. 5, New York. Lawson, T. 2015. Comparing Conceptions of Social Ontology: Emergent Social Entities and/or Institutional Facts? University of Cambridge, Cambridge Working Paper in Economics 1514. Cambridge, England. MacKinnon, D. Dawley, S. Pike, A. and Cumbers, A. 2018. Rethinking Path Creation: A Geographical Political Economy Approach. Papers in Evolutionary Economic Geography, # 18.25, Utrecht University, Urban & Regional research Centre, The Netherlands. Mayhew, A., 2018. An Introduction to Institutional Economics: Tools for Understanding Evolving Economies, The American Economist, 63 (1), pp. 3-17. Manara, V. C. and Sacconi, L. 2019. Institutions, Frames, and Social Contract Reasoning. EconomEtica Working Paper No. 71, Milan, Italy. Michie, J. 2020. The degeneration of capitalism from a system of production to a speculative orgy, International review of Applied Economics, 34 (20), pp. 147-151. Renault, M. 2018. Edmond Malinvaud’s criticisms of the New Classical Economics: Restating the Nature and the Rationale of the Old Keynesians’ Opposition. Department of Economics, University of São Paulo, FEA-USP Working Paper No. 2018-21, Brazil. Schnabel, I. and Shin, H.S. 2018. Money and trust: lessons from the 1620s for money in the digital age. BIS Working Paper No 698, Basle, Switzerland. Schwartz, H. M. and Tranoy, B.S. 2019. Thinking about Thinking about Comparative Political Economy: From Macro to Micro and Back. Politics and Society, 47 (1), pp. 23-54. Shubik, M. 2004. The Theory of Money and Financial Institutions, volumes 1 & 2. Massachusetts: the MIT Press. _________. 2012. The Theory of Money and Financial Institutions, volume 3. Massachusetts: the MIT Press. Stockhammer, E. and Ali, S.M. 2018. Varieties of Capitalism and post-Keynesian economics on Eurocrisis. Post-Keynesian Economics Society Working Paper No. 1813, UK Tubaro, P. 2009. Agent-based Computational Economics: A Methodological Appraisal. Université Paris X Nanterre, Document de Travail No. 2009-42, Paris. Tarullo, D. K. 2019. Financial Reputation: Still Unsettled a Decade After the Crisis. Journal of Economic Perspectives, 33 (1), pp. 61-80. Vahabi, M. 2017. János Kornai and General Equilibrium Theory. Document de travail du CEPN (Centre d’économie de l’Université Paris Nord) No. 2017-16, Paris. Zhang, W-B. 2006. Discrete Dynamical Systems, Bifurcations and Chaos in Economics. Amsterdam: Elsevier. |