Inequality in Marx and Piketty

|

|

6

|

|

by definition and S is total savings. It follows that

and in a closed economy it follows that s = s' ∙ (1+ β).

7 It is worthy to keep in mind that Piketty due his definition of capital underestimates the profit rate and finds a value around 5% on average which is close to the average long-term bond rate.

8 I use the word equivalent because in Marx the ratio of dead to living labour referred to as the “value composition of capital” and denoted by (c/v) is calculated in (labour) value and not physical units like the capital labour ratio (K/L) in the neoclassical production function.

9 It must be mentioned that the definition of capital is much different between the two approaches.

10 When α = 1 we have the unrealistic case where the whole income is profit.

11 This means that productivity (d) and population growth (n) are model parameters. The Goodwin (1967) model solution arrives to the following system of non-linear differential equations:

7 It is worthy to keep in mind that Piketty due his definition of capital underestimates the profit rate and finds a value around 5% on average which is close to the average long-term bond rate.

8 I use the word equivalent because in Marx the ratio of dead to living labour referred to as the “value composition of capital” and denoted by (c/v) is calculated in (labour) value and not physical units like the capital labour ratio (K/L) in the neoclassical production function.

9 It must be mentioned that the definition of capital is much different between the two approaches.

10 When α = 1 we have the unrealistic case where the whole income is profit.

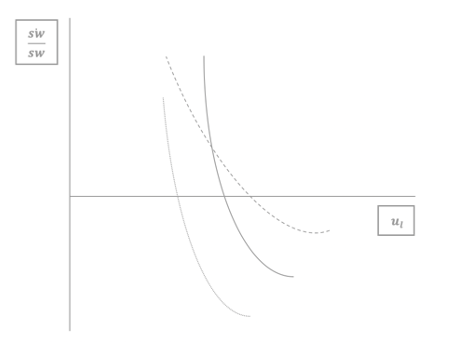

11 This means that productivity (d) and population growth (n) are model parameters. The Goodwin (1967) model solution arrives to the following system of non-linear differential equations:

The first equation is the Goodwin version of equation (25) with constant productivity growth (d) and a linear wage growth employment function

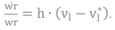

The parameter h is the reaction parameter of wages to an increase in employment and the employment rate vl* is the rate of employment above which wages and the wage share begins to rise. A high value of h and a low value vl* are indications of labour class strength. The equilibrium value of employment is given from the first equation and is:

This means that high labour strength means lower employment. At the same time, the equilibrium wage share given from the second equation is: swe=1-(n+d)∙β (β is assumed constant) which is not affected by labour strength.

12 The eight-hour working day was the central political objective of the 1st International.

13 Although additional empirical investigation is required, it is almost certain that the main source of rising inequality in the neoliberal era is “within-country” inequality. It is for this reason that I confined the Marxist analysis to the “wage share” and the “profit upon alienation”. Of course in the Marxist tradition there is extensive literature explaining inequality through transfers of value between the developed and underdeveloped world. Recent empirical studies are supportive of this literature as well as the approach taken herein. They show high, persistent but constant cross-country inequality throughout the greatest part of the neoliberal era (Lakner & Milanovic, 2015).

References

Acemoglou, D. and Robinson, J. A. (2015). The Rise and Decline of General Laws of Capitalism. Journal of Economic Perspectives, 29 (1), pp. 3-28.

Acemoglu, D., Johnson, S. and Robinson, J. (2005). “Institutions as a Fundamental Cause of Long-Run Growth”. In P. Aghion and S. Durlauf (Eds.), Handbook of Economic Growth Volume 1A (pp. 385-472). Amsterdam: Elsevier-North Holland.

Arrow, K. J., Chenery, H., Minhas, B. and Solow, R. (1961). Capital-Labor Substitution and Economic Efficiency. The Review of Economics and Statistics, 43 (3), pp. 225-250.

Atkeson, A., Chari, V. V. and Kehoe, P. (1999). Taxing Capital Income: A Bad Idea. Federal Reserve Bank of Minneapolis Quarterly Review, 23 (3), pp. 3-17.

Botwinick, H. (1993). Persistent Inequalities: Wage Disparities under Capitalist Competition. Princeton: Princeton University Press.

Chamley, C. (1986). Optimal Taxation of Capital Income in General Equilibrium with Infinite Lives. Econometrica, 54 (3), pp. 607-622.

Dobb, M. (1973). Theories of Value and Distribution Since Adam Smith. Cambridge: Cambridge University Press.

Domar, E. D. (1946). Capital Expansion, Rate of Growth, and Employment. Econometrica, 14 (2), pp. 137-147.

Dragulescu, A. and Yakovenko, V. (2001). Evidence for the Exponential Distribution of Income in the USA. The European Physical Journal, 20, pp. 585-589.

Dragulescu, A. and Yakovenko, V. (2002). Statistical Mechanics of Money, Income, and Wealth: A Short Survey. Available at: https://arxiv.org/pdf/cond-mat/0211175.pdf.

Felipe, J. and McCombie, J. S. (2013). The Aggregate Production Function and the Measurement of Technical Change. Northampton Massachusetts: Edward Elgar Publishing, Inc.

Galbraith, J. (2014). Kapital for the Twenty-first Century. Available at: https://www.dissentmagazine.org/article/kapital-for-the-twenty-first-century.

Goodwin, R. (1967). “A Growth Cycle”. In C. H. Feinstein. (Ed.), Socialism, Capitalism, and Economic Growth. Cambridge: Cambridge University Press.

Harcourt, G. C. (1972). Some Cambridge Controversies in the Theory of Capital. Cambridge: Cambridge University Press.

Harrod, R. F. (1939). An Essay in Dynamic Theory. The Economic Journal, 49 (193), pp. 14-33.

Judd, K. (1985). Redistributive Taxation in a Simple Perfect Foresight Model. Journal of Public Economics, 28 (1), pp. 59-83.

Karabarbounis, L. and Brend, N. (2014 ). The Global Decline of the Labor Share. Quarterly Journal of Economics, 129(1), pp. 61-103.

Kondratieff, N. (1984). The Long Wave Cycle. New York: Richardson & Snyder.

Krussel, P. and Smith, A. J. (2015). Is Piketty’s “Second Law of Capitalism” Fundamental? Journal of Political Economy, 123 (4), pp. 725-748.

Kuznets, S. (1955). Economic Growth and Income Inequality. The American Economic Review, 45 (1), pp. 1-28.

Lakner, C. and Milanovic, B. (2015). Global Income Distribution: From the Fall of the Berlin Wall to the Great Recession. Policy Research Working Paper 6719, The World Bank.

Lucas, R. E. (1988). On the Mechanics of Economic Development. Journal of Monetary Economics 22, pp. 3-42.

Mankiew, N. G. (2015). Yes, r > g. So What?. American Economic Review: Papers & Proceedings, 105 (5), pp. 43-47.

Mankiw, N. G., Romer, D. and Weil, D. N. (1992). A Contribution to the Empirics of Economic Growth. The Quarterly Journal of Economics, May, pp. 407-437.

Marx, K. (1875). Critique of the Gotha Programme. Moscow: Progress Publishers.

Marx, K. (1887). The Capital Vol. I. Moscow: Progress Publishers.

Marx, K. (1894). Capital Vol. III. New York: International Publishers.

Marx, K. (1973). Grundrisse . London: Penguin.

Marx, K. and Engels, F. (1848). The Communist Manifesto. Moscow: Progress Publishers.

Morgan, J. (2015). Piketty’s Calibration Economics: Inequality and the Dissolution of Solutions?. Globalizations, 12 (5), pp. 803-823.

Naidu, S., Rodrik, D. and Zucman, G. (2020). Economics after Neoliberalism: Introducing the EfIP Project. AEA Papers and Proceedings, 110, pp. 366-371.

Phelps, E. (1961). The Golden Rule of Accumulation: A Fable for Growthmen. The American Economic Review, 51 (4), pp. 638-643.

Piketty, T. (2014). Capital in the 21st Century. Cambridge Massachusetts: Harvard University Press.

Piketty, T. (2015). About "Capital in the Twenty-First Century". The American Economic Review, 105 (5), pp. 48-53.

Piketty, T. (2015). The Economics of Inequality. Cambridge Massachusetts: The Belknap Press of Harvard University Press.

Piketty, T. (2018). “Technical appendix of the book « Capital in the twenty-first century»”. In T. Piketty, Capital in the twenty-first century (pp. 1-97). Cambridge Massachusetts: Harvard University Press.

Piketty, T. and Saez, E. (2003). Income Inequality in the United States 1913-1998. Quarterly Journal of Economics,108 (1), pp. 1-39.

Piketty, T. and Zucman, G. (2014). Capital is Back: Wealth-Income Ratios in Rich Countries 1700-2010. The Quarterly Journal of Economics, 129 (3), pp. 1255-1310.

Piketty, T. and Zucman, G. (2014b). “Wealth and Inheritance in the Long Run”. In A. Atkinson and F. Bourguignon (Eds.), Handbook of Income Distribution. Vol 2B (pp. 1303-1368). Amsterdam: North-Holland.

Rosdolsky, R. (1977). The Making of Marx's Capital. London: Pluto Press.

Shaikh, A. (2016). Capitalism, competition, Conflict, and Crises. New York: Oxford University Press.

Shaikh, A. (2016). Income Distribution, Econophysics, and Piketty. Review of Political Economy, 29(1), pp. 18-29.

Silva, C. and Yakovenko, V. (2004). Temporal Evolution of the “Thermal” and "Superthermal” Income Classes in the USA from 1983–2001. Europhysics Letters, 3 (31), pp. 1-7.

Solow, R. M. (1956). A Contribution to the Theory of Economic Growth. The Quarterly Journal of Economics, 70 (1), pp. 65-94.

Solow, R. M. (1957). Technical Change and the Aggregate Production Function. The Review of Economics and Statistics 39 (3), pp. 312-320.

Stolper, W. and Samuelson, P. (1941). Protection and Real Wages. The Review of Economic Studies, 9 (1), pp. 58-73.

Yakovenko, V. (2007). Statistical Mechanics Approach to Econophysics. Available at: https://arxiv.org/abs/0709.3662.