Financing obstacles to the realization of 21st century socialismVictor van den Werdeen

Abstract

In the following paper I introduce a 21st century alternative to the modern neoliberal economics order. I call such an alternative “21st century socialism” whose defining feature is the organization of all economic production through labor-managed (LMF) as opposed to capital managed firms (KMF). Such LMFs are characterized by democratic control of economic production by all those involved in the production process on the basis of one man-one vote. If such an economic system can be proven to be theoretically viable then it presents a real alternative to contemporary capitalism. However, in the literature one key obstacle to the formation and viability of LMFs has been identified: the lack of access to cost-efficient financing in the startup phase and inefficient investment decisions once the firm has come to exist. In the following paper, we examine the nature of these financing difficulties and hint at a possible solution. Keywords: socialism, neo-classical theory of firm, labour-managed economy JEL classification: P16, P31, B14, B51 1. Introduction In line with the theme of the current issue of the journal: “the world in transition: the great recession, conflicts, and imperialist rivalry in the 21st century”, this paper attempts to give a detailed analysis of an alternative form of economic organization to the dominant capitalist controlled firms of modern neoliberal economies. These hierarchical bastions of authority have always served as locus of conflict between capitalist and laborers since the Industrial Revolution. An LMF economy, or an economy of labor-managed firms would offer the true 21st socialist alternative to modern capitalism in reversing what Jossa (2014) calls the fundamental hiring relationship of capital and labor in capitalist economies; instead of capital hiring labor, labor now hires capital. The success of a complete labor-managed economy (LME) such as that envisioned by Jaroslav Vanek (1975) will of course depend on the existence of what Vanek calls “support structures” such as a national planning agency and a cooperative banking system. Nevertheless, it is worth examining the economic viability of such an economy, independent of the institutional context, and within the frames of orthodox economic theory. For if such firms can be shown to be viable even in the neoclassical fantasy world then orthodox economists have no effective strategy to challenge LMFs within the rhetoric of mainstream economics. The macroeconomic implications of an LME are beyond the scope of this paper, but the theme of the current journal issue invites us to reflect on the implications that an LME would have for imperialist rivalry. If imperialism is the characteristic and inevitable consequence of global capitalism as Lenin argued, then surely imperialism would not exist within the confines of a socialist system. For labor is distinguished from capital in one fundamental respect, capital is alienable and impersonal hence it has no bond or connection to any territory or land. It does not discriminate in its ruthless pursuit of profit. Labor on the other hand is the only uniquely human input and hence any decisions made by an LMF will take into account the welfare of the collective labor force when making economic decisions. And since laborers tend to reside in the areas they world, LMFs will also encourage greater concern for the welfare of the greater community even outside the employees of the firm. If the natural consequence of the spirit of solidarity and community engendered within the workplace is the spread of such a spirit throughout one’s society and eventually other societies, then an LME can be seen as a potential antidote to zero-sum imperialism as the collective of workers eventually becomes the collective of all the world’s laborers; thus the interests and the collective welfare of the entire working community will become the sole goal of all economic organization. As was said, labor-managed firms have long been invoked throughout history as a potential alternative paradigm to the hierarchical capital managed firms which define and dominate capitalist economies, even more so within the current epoch of neoliberalism. However, the potential for such labor-managed firms or LMFs to undermine the economic status quo of giant capital-managed corporations, depends on the economic viability of such organizations in the real world. Financing difficulties are frequently invoked in the LMF literature as one of the principal reasons accounting for the rarity of LMFs relative to KMFs. In this paper we will explore how financing difficulties plague LMFs in both the initial startup phase and once they have already come into existence. The financing difficulties which affect LMFs can broadly be classified as issues of underinvestment and occur with all classes of LMF financing: leasing, bond financing, and equity financing. If labor-managed firms are ever to challenge the central pillar of neoliberalism, control by unaccountable financial and monopoly capital instead of economic democracy, an effective solution to the LMF underinvestment issue must be found, which may require the use of a new class of financial instruments broadly taking the name, ‘quasi-equity’. 2. Financing difficulties as an obstacle to LMF emergence Neoclassical theories of labor-managed firms state that in a world of complete and perfectly competitive markets KMFs and LMFs would be symmetrical in their static and dynamic behavior. Such ‘equivalence theorems’ show that an economy of labor-managed firms will be as allocatively efficient as an economy of capital-managed firms (Dreze 1976, 1989, Dow 1996). The natural question that arises then is: if LMFs are as efficient as KMFs why do they occupy only a marginal place in Western market economies? Although there is no consensus answer to this perplexing question, the last four decades of research on the economics of LMFs has more or less converged on financing difficulties as the key barrier to the spread of LMFs in Western market economies. For example, Jacques Dreze asserts that “funding difficulties are the main reason why labor-managed firms are not spreading within capitalist economies” (1993, pg. 261). Specifically, the financing problems of LMFs enter at two points: before the LMF is created and once the LMF is already in existence. The first point of entry for LMF financing difficulties involves a combination of low worker wealth with credit rationing in bond markets and non-voting equity markets which hamper the rate at which workers will pool resources to form LMFs (Dow and Putterman 2006). The second point of entry for financing difficulties plaguing LMFs is once such firms have already come into existence. The principal financing difficulty affecting incumbent LMFs is the much discussed ‘underinvestment’ phenomenon which leads first to depressing the private value per unit of capital of the LMF and hence the growth rate of the LMF relative to the KMF and secondly to the increased likelihood that worker-members of existing LMFs will sell their firms to capitalist investors (Dow 1993). In evolutionary terminology the first point of entry for funding difficulties is the lower rate of differential birth of LMFs as such firms have major difficulties getting off the ground. The second point of entry is the higher rate of differential death of LMFs relative to KMFs as underinvestment issues threaten slower-growing LMFs from being outcompeted by KMFs in competitive markets, resulting either in bankruptcy or degeneration into an investor controlled firm. In order to make sense of the increased funding difficulties that LMFs face relative to KMFs during the formation stage it is necessary to invoke what Dow (2003) calls a “symmetry principle” which traces symmetrical behavior of LMFs and KMFs back to qualitative symmetries (in both a physical and institutional sense) of labor and capital inputs (pg. 118). The obvious corollary of such a “symmetry principle” is that any asymmetrical behavior between LMFs and KMFs must be ultimately derived from some qualitative asymmetry between capital and labor. The asymmetrical behavior of LMFs is evident from the fact that they are rare relative to KMFs and the fact that LMFs are seldom found in industries with large economies of scale, high capital intensity, or highly specialized physical assets. The fundamental asymmetry between capital and labor inputs can be termed the ‘alienability’ characteristic. The alienability of capital implies that the ownership of non-human assets can be shifted from one person to another while endowments of labor-time and skill cannot (ibid). Williamson (1985) likens this asymmetry to the difference between stocks and flows; while capital can provide its whole self to the firm as a stock labor can only supply a service flow. The fundamental asymmetry between labor and capital inputs is the source of the causal channel through which one potential cause (on the differential birth side) of LMF rarity can begin to be explained. The causal explanation of LMF rarity begins with a contingent fact which nonetheless is of enormous significance. The contingent fact is that on workers tend be suffer from limited wealth and liquidity constrains so the lack the resources needed to finance jointly owned assets. Using back-of-the-envelope calculations data from 1988 Bowles and Gintis (1996) estimate that the average net worth of the least wealthy 80 per cent of American workers (half of which was tied up in homes and cars) was about $64,000 while the capital stock per employee was about $95,000. Thus the typical net worth of a worker is about half the value of the capita stock they typically work with. For this reason workers will have to rely on leasing, debt financing, or equity financing if they are to purchase the physical assets which will constitute the firm. As was established above capital is an alienable stock while labor is an inalienable service flow. Stocks can be leased and owned while service flows can only be leased. Leasing of capital assets as a cost-effective option for firms was ruled out in the beginning as costly information (information is costly to obtain and transmit) and asset specificity lead to costly monitoring of service flows and the threat of quasi-rent expropriation respectively (Alchian and Demsetz 1972 and Klein, Crawford, and Alchian 1978). Thus workers interested in creating a labor-managed firm will have to rely either on bond (loan capital) financing or equity (risk capital financing) to finance the firm’s capital assets. In this scenario then an upfront investment of capital must be provided in exchange for future interest payments in the bond financing case or future dividend payments in the equity financing case. But once the stock of alienable capital has been committed, the LMF may be able to rely solely on internal financing from retained earnings for working capital and maintenance thus eliminating the need for the LMF to dip back into equity and bond markets (Dow 2003, pg. 237). Members of the LMF will thus face a problem of making “credible commitments” to capital in order to ensure investors that the LMF will not take advantage of an upfront capital investment by paying themselves higher wages, depreciating assets, or pursuing risky projects (ibid). The threat of non-renewal by investors has little force if assets are durable, retained earnings are healthy, or the firm is on the verge of bankruptcy. Such situations characterized by a divergence of incentives between principal (lenders) and agent (worker-borrowers) are termed ‘moral hazard’ problems, scenarios where the agent takes more risk since the principal bears the costs of these risks. Moral hazard problems involve ex post asymmetric information. Only after the contract has been created to informational asymmetries enter into the picture as the principal can neither control or costless verify the level of risk which the agent may undertake. Gui (1985) confirms the above moral hazard dilemma in the bond market arena as agent/worker liquidation (bankruptcy) depends on the realization of a stochastic variable, gross income from production (value-added inclusive of capital costs) which is only observable to the worker-members. Workers (agents) can thus liquidate projects to avoid debt repayment which the lenders (principals) have no way of anticipating in situations of asymmetric information. Moral hazard dilemmas where informational asymmetries are ex post should be contrasted with so called adverse selection problems where informational asymmetries are ex ante, appearing even before the loan contract between principal and agent is signed. For example, if some borrowers have better skills or projects than others but lenders cannot distinguish between different quality projects ahead of time then borrowers will find it difficult to convince lenders that the probability of loan repayment is sufficiently high, leading to prohibitive interest rates and credit rationing once again. Symmetrically, adverse selection problems may also affect groups of workers who when confronted by a wealthy investor who offers to transfer his assets through a debt contract, cannot confirm the quality of the investor’s project beforehand (Dow 2003, pg. 209). To make matters worse because workers are poor they lack the funds necessary to make so called “trust investments” in their own projects which would signal to lenders or equity investors the likelihood the project succeeding. Furthermore because human capital is inalienable workers cannot offer their own future labor income as collateral that would be forfeited to banks in case of default (Hart and Moore 1994). Even if the Sertel-Dow market for membership rights is introduced, due to prohibitions on indentured servitude and the illiquidity of individual claims on the LMF’s capital assets, it will be difficult to secure a loan using the membership right as collateral (Dow 1993, pg. 192). The overall outcome of the LMF’s inability to make credible commitments to capital are high interest rates or outright credit rationing in the case of bond financing or a higher cost of capital (selling stock at a cheaper price) reflected in higher returns demanded by equity financiers (Stiglitz and Weiss 1981). Bowles and Gintis (1993) correctly stress the contested nature of exchange in bond markets as the promise by the borrower to repay the lender is enforceable only if the borrower is solvent at the time repayment is due, and the borrower’s promise to repay is not amenable to third-party enforcement (pg. 32). The incentive incompatibility between creditors and borrowers is heightened by the fact that since workers receive employment rents, they profit from the firm’s continued operation even when the future profits are expected to be negative whereas lenders will prefer that the LMF declare bankruptcy in such a situation (Gintis 1989). Equity financing in the case of the LMF can only be of the non-voting equity type as granting owners of capital (even if they are workers) votes on the basis of the amount of capital supplied contradicts the fundamental tenet of worker self-management: one member one vote. Lack of worker wealth thus combines with the inability to make credible commitments to capital to make external financing for LMFs a bleak and costly option. As Hodgson (1996) indicates such an obstacle as costly access to external financing could ensure that labor-managed firms are less numerous than hierarchical firms, even if in the best case scenario they suffer no efficiency disadvantages, because they are less likely to emerge in the first place. If the financing troubles which LMFs will face are as gloomy as concluded above then “…hierarchical firms may grow in size or number to swamp the non-hierarchical businesses, whatever the relative efficiencies” (ibid, pg. 103). It is important to stress that KMFs can in theory face the same difficulties in making credible commitments to capital that LMFs face. As Dow (2003) points out “…there are no data comparing the cost of external capital for KMFs and LMFs so it is impossible to determine directly whether LMFs are disadvantaged in the credit market relative to similar KMFs” (pg. 192). The fundamental difference, however, is that capital suppliers are wealthier than workers so they do not have to rely as much on incomplete capital markets to finance their firms and when they do go to capital markets for financing their higher level of wealth allows for financing on less costly and more favorable terms. Capital suppliers and the KMFs which they form, while facing less of the problem of making credible commitments to capital, are subject to the symmetrical problem of making credible commitments to the workers whose labor service flow they lease. But just because labor time is a service that is leased and not a stock to be bought there is an increased incentive to protect their reputation in the eyes of workers as KMFs will frequently have to dip back into the labor market to replace labor services lost through worker turnover. To summarize the overall flow of the channel from labor-capital asymmetry to a lower emergence rate for LMFs the causal chain can be conceived of as thus:

From the above flow chart it can be seen that the major causal factor (indicated by the bold arrow) which lead to the difficulty of making credible commitments to capital are the fact that capital is alienable. The other two factors, low worker wealth and the fact that inalienable human capital cannot serve as collateral, are best seen as auxiliary causes of low credibility commitments to capital. The orange color of the arrow leading from low worker wealth to entry of worker-members into capital markets is intended to show that the initial situation of low worker wealth is merely the trigger which begins but does not cause the flow of the causal channel from capital-labor asymmetry through lack of credible commitments to costly financing and low emergence. To repeat bold arrows indicate the flow of the causal channel while the orange arrow is only the trigger.

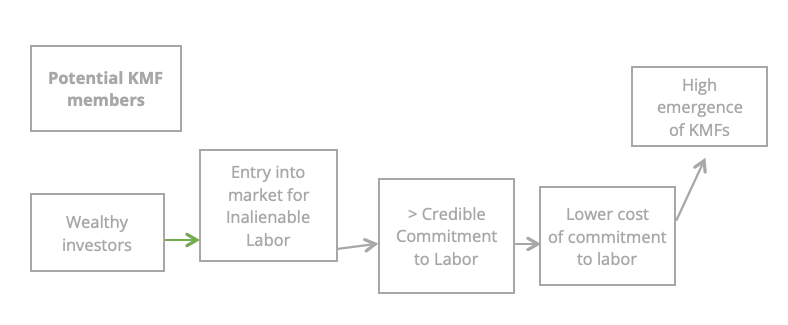

The symmetrical causal channel for the KMF can be summarized by the following flow chart.

In contrast to the scenario facing potential LMF members, a high level of wealth for owners of substantial capital triggers their entry into the market for inalienable labor-power to which they can make a more credible commitment to (for the reputational reasons outlined above), leading to lower transaction costs in contracting labor, and ultimately a higher emergence rate for the KMF form. The qualitative asymmetry between labor and capital as pertains to the credibility of commitments to labor and capital can be put another way. While labor, since it is inalienable, can always pick up and leave if it is not satisfied by capital’s promises, capital, as an alienable stock, does not have the same freedom to pick up and leave once it has been given to labor. As regards the differing costs of reputations for labor and capital respectively, while capital has to return frequently to the labor market since labor is always free to pick up and leave, once capital has been given over to labor, labor does not have to return to the capital market again as long capital remains firmly in its hands!

3. Underinvestment in the WMF. LMF*, and PC Up until now we have been discussing the first point of entry for the financing difficulties faced by LMFs as a general category. In the following section we will be looking at the second point of entry for LMF financing difficulties; specifically, the issues of underinvestment which arise once self-managed firms have already come into existence. To continue with the evolutionary analogy, underinvestment issues in incumbent LMFs deals with the differential death (survival value) of such firms rather than their relative fecundity or probability of emergence. The central underinvestment issues which are attributed to self-managed firms in LMF financing literature are: the ‘Furubotn-Pejovich effect’ or horizon problem , the ‘Vanek effect’, and the risk-sharing effect. Briefly, the Furubotn-Pejovich effect (first discussed by Pejovich (1969), Furubotn and Pejovich (1970), Furubotn (1971, 1976)) refers to the tendency of WMFs to underinvest when the time horizon within which worker-members expect to remain with the firm is shorter than the time period over which they will see the full returns on investments made from retained earnings. The reason for this ‘horizon problem’ is rooted in the fact that once partners of WMFs leave their firms they forfeit any rights to both the principal of their investments, the value of any assets created out of retained earnings, and any returns, reflected in the higher future dividends per worker resulting from the initial investment (Jossa 2014). The second financing problem encountered in the LMF literature is the so called ‘Vanek effect’ or the ‘self-extinction’ force (Vanek 1977). The ‘Vanek effect’ occurs when LMFs are financed exclusively from retained earnings (or internal financing) leading to the following distorting ‘forces’: (1) firms operate in the increasing returns to scale zone of production (output is too low) as the marginal product of labor lies above the level of the typical worker’s marginal rate of time preference, (2) at any given level of capital the firm will attempt to reduce membership, (3) the gradual disinvestment and capital consumption undertaken in order to achieve the desired capital/output ratio, and (4) adjustments to the capital/labor ratio are always carried out by varying capital and never by increasing membership (George 1990, pg. 12). Vanek hypothesized that an LMF financed through retained earnings will become extinct over time because of the four forces listed above. The final category of financing perversities plaguing self-managed firms (LMFs) are classed as “risk-sharing effects”, and refer to the problem of optimally allocating risk between workers and investors when LMFs are exclusively funded out of loan capital (external financing). The fundamental problem of optimal risk-sharing involves the purported conflict between risks and incentives within the Vanek LMF*. Full-debt financing protects workers from bearing the lower tail of enterprise risk through default (thus avoiding bond repayments) while allowing them to capture the upper tail of any extraordinary gains (McCain 1977). But if the worker’s income is insured against such firm-specific risks via transferring the risk to lenders then they will have less of an incentive to repair and maintain the capital assets financed through loans in order to extract as much current income from its use as possible (Jensen and Meckling 1979). On the other hand if workers as residual claimants are made the equity-owners of their capital assets then they will have an incentive to optimally use and maintain the assets. But if the majority of assets are financed out of the workers’ equity then the worker shareholders could potentially lose all of their invested wealth as after liquidating the firm’s assets, creditors and bondholders are paid before equity investors who might only scrap up a tiny residual in the realm of pennies on the dollar. Such a risk is amplified in the case of worker-owners who cannot diversify their portfolios by holding several membership rights in several firms. Having analyzed how the WMF is plagued by both the Furubotn-Pejovich effect and the Vanek effect, it is now time to consider the investment behavior of that particular LMF, LMF* as we have called it, that is financed exclusively through bonds/loans or what Vanek (1975, 1977) calls external financing. Like the WMF but unlike the Western style PCs, partners of the LMF* lack individual property rights to firm’s capital goods or assets, as the assets are collectively owned to use the terminology introduced above. Although LMFs* are prohibited from internal financing, in the sense of financing from retained earnings, there is nothing prohibiting such firms from loaning capital from its own members. Partners who choose to invest their private savings in debentures (an unsecured bond) of the firm, are granted the same rights as any holder of a debt security: the right to enjoy interest, to recoup the loaned capital on maturity, and to be able to sell the bonds at any moment on financial markets. Because an externally financed LMF* can sell bonds to its own internal constituents, Jossa (2014) rightly concludes that the internal vs. external financing distinction is the wrong line of demarcation to draw. Rather, he proposes that the distinction between a LMF* and a WMF should be drawn on the basis of LMFs which distinguish between labor income and capital income and those that do not. Labor income is taken to mean the average net income that a worker receives in virtue of his being a member of the firm while capital income is the return on capital accruing to holders of equity (dividends), bonds (interest rate), or leasing agreements (capital rental rate). A WMF, which is financed through retained earnings, makes no such distinction between capital and labor income as the income which partners receive derives both from their status as workers in the firm (with the corresponding right to the net income) and as contributors of capital, who accept reductions in dividends in order to finance fresh investments; dividends paid out from future retained earnings will thus reflect the new increased value of the firm’s assets in addition to the worker’s regular right to a share of the firm’s profits. Returning to the financing issues faced by self-managed firm type LMF*, because the LMF* is exclusively financed from loan capital (whether the holders of the debentures are themselves partners or not), the partner’s contribution to capital investment out of retained earnings is zero and hence there can be no Furubotn-Pejovich effect (Jossa and Cuomo 1997). Jossa (2014) argues that the LMF*, although not exhibiting the F-P effect, may have a tendency to exclude efficient investments, which a profit-maximizing (PMF) twin would undertake, because lacking the ability to recover any part of capital LMF* members will only take into account the future income that will flow from the investment and not any variation in the firm’s net worth. As is well known, in a PMF a precondition for undertaking an investment project is that the internal rate of return (IRR), the discount/interest rate at which the net present value (NPV) of all cash flows is equal to zero, is greater or equal to the minimum acceptable rate of return (MARR), the minimum rate that the firm expects to earn when investing in the project (or the firm’s weighted average cost of capital (WACC)). Equilibrium is reached when the IRR is equal to the MARR or:

where RL is the annual gross income from the investment, r is the interest rate, t is any year, T the terminal year of the project, and C0 is the purchase price of the machine or cost of capital. Jossa and Cuomo (1997) state the equilibrium condition of the marginal investment of one monetary unit as following:

where the left-hand side of the equation represents as above the NPV of the future investment returns and the right-hand side is the cost of the investment equal to one monetary unit. In an LMF* where the worker-members do not bear the reductions in the capital value of the assets and whose only cost is to reimburse the bondholders with a quota of capital increased by the matured interest (principal plus interest), face a different investment constraint than both the PMF and WMF. However, even though the underinvestment effect facing an LMF* is different than the F-P effect which plagues the WMF, both result from the potentially truncated time horizon of the partner. In the case of the LMF* the limited time horizon of partners leads to a distortionary effect on investment decisions which can result not only in underinvestment but a kind of “overinvestment” (Jossa 2014). A point of clarification is in order here. Jossa claims that the LMF* will experience a form of overinvestment if a project that is deemed inefficient in the long run but efficient during the time horizon of the partner is undertaken. However, it suffices to say that such projects even though they yield temporary efficient returns, will lead to a decrease in the total net worth of the firm in the long-run and hence remain an instance of underinvestment when seen in their totality. To see why an LMF* is said to make inefficient investments consider the investment constraints facing members of the LMF*. According to Jossa and Cuomo (1997) partners of the LMF* whose time horizons are shorter than the duration of the investment will have an incentive to make the marginal investment as long as:

where n is numbers of years the majority partner expects to remain with the firm, rt the gross return on investment, dt the annual rate of depreciation of investment, and it the market interest rate. Equation (3) states that the investment will only be made when the cost of investment represented by the depreciation and interest on loaned capital is equal to the returns on the investment. If n is shorter than the duration (in years) of the investment, T, then the partners of the LMF* have an incentive to make inefficient investments. That is to say, because the partners of the LMF* are only concerned with equalizing the flow of costs to the flow of returns in the years 1 to n, they will neglect the marginal investment constraint in the period from n + 1 to T. Because of the truncated time horizon, the members of LMF* will take on projects which on the whole are inefficient (the flow of costs is greater than the flow of returns), but within the years 1 to n are efficient. In contrast, WMF members (like members of PMFs) will never undertake inefficient investments as they have a vested interest in recovering the entire cost of capital, which they contributed through retained earnings not paid out in dividends (self-financing). The WMF will thus only undertake the marginal investment if equation (4) is satisfied:

If the time period which the worker-members expect to remain with the firm (n) is shorter than the period in which the investment will provide returns (T) then the WMF experiences the F-P effect, with partners suffering a loss “…equal to the difference between the reduction of the dividends and the returns on the investment already obtained and withdrawn” (Jossa and Cuomo 1997, pg. 213). Formally a WMF experiencing the F-P effect will make a loss P on the marginal investment where:

Thus a WMF member will use the marginal investment rule (4) instead of (3) which is employed by the profit-maximizing firm (PMF). Given n is less than T the internal rate of return of the WMF will be smaller than the PMF and hence WMFs exhibit the well-known tendency of underinvestment which has been widely discussed in the literature (Stephen 1984, Vanek 1975, Bonin and Putterman 1984). Jossa (2014) is correct to point out that the ‘Furubotn-Pejovich’ underinvestment effect is used rather loosely in the literature. He points out that the F-P may refer to two distinct underinvestment forces operating in the WMF: (1) partners forfeit their rights to a share of returns on the investment upon leaving the firm but are not denied reimbursement for their past capital contributions made through dividend reductions when the investment project is completed and (2) in addition to forfeiting their rights to the firm’s net income the worker collective as a whole is prohibited from reimbursing partners through depreciation expenses due to ‘capital maintenance requirement’ (CMR) requiring WMFs to replace worn-out equipment and hence at a minimum to maintain the total value of capital assets at all times (Jossa 2014). To be clear, in a WMF workers do not the right of refund of their capital share at the time of their withdrawal given that they have no corresponding claims on the net worth of the firm upon leaving. They do however have an incentive to recover the past dividend deductions made for reasons of self-financing, during their tenure with the firm through cashing in on the returns to the investment. A CMR ensures that not only is the right of refund forfeited but any possibility a partner had of recouping his share of the past self-financed investment.

Returning to the LMF*, it was concluded that such firms have a tendency to make inefficient investment decisions, arising from a distorted investment rule (3) where the time horizon (n) of the partner replaces the lifespan of the investment (T) in the upper limit of summation. The truncated time horizon of the LMF* member is a necessary but not a sufficient condition for the occurrence of inefficient investments. The sufficient condition for inefficient investments, which was alluded to above, is that LMF* members have an incentive to delay depreciation of externally financed capital goods. More specifically, since members of the LMF* do not have a right to the capital assets of the firm upon retirement they will not take into account the full cost of the investment (reductions in the capital value of assets). Nothing changes when LMF* partners are the ones who acquire bonds and become the firm’s creditors, as the fact remains that no has a right to the net worth of the firm upon departure. Every partner in the LMF* thus has an incentive to squeeze as much profit out of the firm’s net worth as long as they remain with the firm without any regard to the firm’s net worth once they retire. Depreciation of course refers to the process of allocating the costs of capital goods over their useful life and can either be done of the basis of matching the depreciation expense (the wearing out of the asset) to its contribution to production, or distributing the depreciation expense evenly across the lifespan of the capital good (straight-line depreciation), or attributing the entire cost to one year. Unlike the LMF*, members of the PMF and the WMF have an incentive to amortize (depreciate) the entire cost of the investment during the investment’s lifetime. Consequently, for the PMF in equation (2) and the WMF in equation (4) 1 = dtT or in other words the total depreciation expense of the capital asset whose life is T years is equal to the initial monetary cost of the investment 1. For an LMF* the investment rule described by equation (3) can be rearranged as:

yielding the equivalence between the gross return on the investment and the cost of the loaned capital whose two components are depreciation dt and itinterest . When n < T, however, the members of the LMF* will have an incentive to delay amortization (fail to attribute depreciation expenses in accordance with asset use) in order to collect non-realized (future) profits yielding the inequality between the attributed costs and interest payments and the full monetary cost of the investment:

where n < T

Thus, unlike the WMF and PMF, the LMF* will undertake an investment even if the net return is less than its total cost so long as the net return of the investment during the n horizon is greater than the flow of costs in the same time period:

Jossa and Cuomo (1997, pg. 227) show that equation (3) can be transformed into a ‘profit equation’ which only looks at the flow of costs and returns in one year:

where rpK is the gross return on depreciation, dpK the contribution of the capital asset to the productive process, and ipK the interest on the loan capital. Jossa and Cuomo (1997) show that if mpK, the share of the value of loan capital pK which is reimbursed to the bondholders on a yearly basis, is less than dpK, or in other words if the attributed cost of capital (the depreciation expense) is less than the average return of capital, then LMF* members in time period t can distribute among themselves the higher dividend D' which represents the non-realized profits due to LMF* members in time period t + 1. Self-interested partners of the LMF* can reimburse bondholders at a lower rate than the rate at which capital goods are worn out and thus leave future LMF* members with the burden of a flow of investment costs (a higher mpK) which is larger than the flow of capital services resulting in lower average dividends for the would-be members. Jossa and Cuomo (1997)’s assertion that LMFs* have an incentive to undertake inefficient investment projects, which can result in underinvestment (including short-term “overinvestment”), is similar to the worry raised by Klein, Crawford, and Alchian (1978) that LMFs who lease their capital assets will have an incentive to wear them out as fast as possible (reducing depreciation expenses) in order to maximize present earnings.

Having looked at the investment shortcomings which in theory plague the WMF and LMF* but no the PMF, it worth looking at a third form which an LMF can take: the Western-style producer cooperatives (PCs). Following Putterman (1990), Ellerman (1992), and Jossa and Cuomo (1987) I will define a producer cooperative as an LMF where the net worth of the firm is contained in individually-owned, internal savings accounts or‘ internal capital accounts’ and individual bonds (like in the LMF*) are paid scarcity-reflecting interest rates. To use Dow’s distinction, PCs are characterized by individual rather than collective asset ownership and may or may not issue individually owned membership rights (shares). Internal capital accounts (bearing the market interest rate) are credited with: any initial capital contributions made by the partners upon joining the PC, the quota of annual profits (either distributed equally or in accordance with the member’s labor contribution), and any retained earnings which were not distributed as dividends but used to finance investment projects. The account is debited when withdrawals of agreed dividends are made by partners. Upon termination the individual capital accounts are closed and paid out to departing members in perpetual bonds which they member can either hold to collect interest or sell in a market for debt securities, either way recouping the full value of past contributions made to self-financing (Ellerman 1986, pg. 64). PCs will clearly not suffer from the F-P effect as all of the firm’s retained earnings which were converted into venture capital (deducted from the partners’ dividends) are reimbursed to the individual partners upon departure. Unlike the WMF, in the PC the right of reimbursement of contributed capital is never touched so there is no incentive for the partner to recuperate the invested capital before leaving the firm. A reduction in the value of the partners’ capital accounts can only occur during their tenure with the firm if the enterprise experiences a downturn in business leading to a decrease in the total net income. Although not experiencing the F-P effect, the PC unfortunately suffers from the same tendency to make inefficient investments as the LMF* does when a partner’s time horizon is less than the duration of the investment project ( n < T and, paradoxically, just because partner’s have a right to the reimbursement of past capital contributions (Jossa and Cuomo 1997, pg. 231). Because partners know they will be reimbursed for their capital contributions unconditionally , they have the same temptation as partners in the LMF* to delay amortization of capital and hence expropriate the profits from future would-be partners leading to a decrease of the firm’s net worth in future periods. The potential for adopting inefficient projects leading to underinvestment in the long run is always lurking in the minds of the PC members as it is with members of the LMF*. 4. Saleable LMF Membership Rights: The Sertel-Dow proposal So if producer cooperatives with internal capital accounts and labor-managed firms with 100 per cent bond financing both face the prospect of inefficient investments is there a way out of this financing quagmire? Dow pinpoints the crux of the problem when he makes clear that the problem with internal capital accounts is that members cannot capitalize on the present value of future investment returns (2003, pg. 155). Just as a market for membership rights was employed as a solution (albeit one among several) to the labor supply perversities discussed in the earlier chapter so Dow (1996, 2003) and Sertel (1982) propose tradeable membership rights as a solution to the underinvestment problems of the WMF, LMF*, and PC. A (perfect) market for membership rights mimics the stock market employed by joint-stock KMFs as every decision made by the firm reflects on the value of the members’ shares, effectively making the time horizon of the partner equal to infinity. The Sertel-Dow labor-managed firm (SDLMF) thus follows the same investment rule as the PMF:

which implies the further rule that the entire value of capital be amortized over the course of its lifetime, so that:

This is the same constraint which both the LMF* and PC violate due to their myopic investment decisions. Earlier, it was mentioned that according to Dow individual membership rights are compatible with both collectively owned capital, owned by the firm qua legal entity, as well as individually owned capital, either in the form of individually owned machines or as in the case of the PC individually owned capital accounts. Saleable membership rights although not logically incompatible with internal capital accounts, make such accounts redundant as the present value of future net income already includes the value of the firm’s net income upon the partner’s departure. Furthermore, tradeable membership rights are compatible with any of the various forms of financing, specifically bonds, non-voting equity shares, retained earnings, or (what will become relevant later on) quasi-equity shares. While the WMF could only finance investment projects out of retained earnings and the LMF* by selling bonds, the entire buffet of financing methods is available to the SDLMF. The PC has the same flexibility in choosing its financing instruments as the SDLMF but it is still hampered by the inability to capitalize returns on investments that extend beyond its partner’s tenure with the firm.

In searching for a possible solution to the inefficient problem facing the LMF* and PC, outlined by Jossa and Cuomo (1997), it is worth investigating further the potential for tradeable membership shares to alleviate the aforementioned problems. Jossa and Cuomo (1997) and Jossa (2014) of course disagree with Vanek (1977) who sees no potential for the LMF* to take on inefficient investments. Because Vanek (1977)’s conclusions are based on the highly idealized assumption that “…capita has infinite durability, and thus there are no problems of depreciation…”, we will use the less restrictive LMF* model outlined by Jossa and Cuomo as our reference point. Moreover, since the LMF* and the PC exhibit identical investment behavior it will suffice to compare the 100 per cent bond financed LMF* with the SDLMF. Lastly, even if the relative merits of tradeable membership rights outweigh their shortcomings, it must still be established which of the various financing instruments outlined above allocate risk between worker and investor in the most optimal way. The “risk-sharing effect”, which is the third class of financing issues faced by the LMF, is paramount in determining the cost of finance, reflected in the size of the risk premium demanded by investors and, if tradeable membership rights, are issued on the price such shares can fetch on the market. As is well known, a higher debt-to-equity ratio (D/E) results in a lower share price and hence an increased cost of financing for a firm who must entice investors with lower earnings per share (E.P.S) (Banks 2007). The first set of criticisms of LMF membership markets comes from Jossa and Cuomo (1997) and has more to do the potential of such markets to undermine the fabric of the LMF as a ‘cooperative’ enterprise. According to Meade (1972) in order to qualify as a cooperative enterprise two rules must be followed: (1) new members will only be taken on board if (a) the new member voluntarily wishes to join and (b) all (or possibly a majority of) the older members accept the new member; (2) incumbent members can only leave the firm if (a) the member wants to leave voluntarily and (b) all/a majority of incumbent members agree to his departure (pg. 414). Jossa and Cuomo’s main worry is that a free market in membership rights would violate (1b) and (2b) as the collectivity would forfeit the right to decide who they can let in and out of the firm. But such an argument borders on strawman territory for Sertel (1982) recognizes that if a membership market is to be workable, then partnership deeds can only be transferred within regions of productive substitutability so a plumber will replace an electrician (pg. 14). To counteract Sertel’s problem Dow recommends that instead of membership rights being sold directly to prospective replacements they are sold first to the firm so that insiders as a collective can internalize quality effects when selecting a replacement (2003, pg. 160). Thus there is no reason to think that a market for membership rights violates Meade’s rules for a cooperative organization. The second set of criticisms of a market for membership rights comes from Dow himself and have to do with the feasibility of implementing such a LMF share market in the real world. The limitations of a market of LMF control stems from the very same inalienability of labor which was said to account for the difficulty workers experience in procuring financing to create their own LMFs. Since membership shares in the LMF are tied to the inalienable labor power of a worker, it is impossible to transfer a membership right to another worker without also replacing the labor service of the initial departing member. The market for LMF control will thus be subject to the same frictions as the labor market in a capitalist economy including: the fact that most workers can only hold one job at a time due to travel costs, workers tend to change jobs infrequently due to the costs of search, turnover, and relocation, and the fact that labor services are heterogeneous with different jobs requiring different sets of skills (Dow 2003, pg. 158). The upshot of these labor market imperfections is that a market for membership rights, unlike a stock market, will only become active and bring efficiency gains if there is a job opening while simultaneously someone else is looking for a job, and secondly that several membership markets will arise for every occupation which requires a qualitatively different set of skills. Imperfect markets for membership rights have a danger of becoming too numerous and when they do exist will be thin and non-market clearing. Dow (1993) links the imperfection of membership markets to underinvestment of LMFs since a failure of incoming members to pay an entry fee equal to the full private value of membership will lead to an undervaluation of future investment returns for incumbent LMFs (pg. 191). The primary factors which prevent membership fees from being bid up to market-clearing levels include the combination of low worker wealth with credit rationing (which we pinned down earlier as the channel through which the creation of LMFs is impeded), the lack of government unemployment insurance to protect risk-averse workers, with undiversified portfolios (workers can only usually hold one membership right unlike the unlimited number of shares available to stock market investors) from periods of economic downturn, and the adverse selection problem which arises when asymmetric information prevents outsiders from ascertaining the true expected future value of the firm which insiders know but have no incentive to disclose. Furthermore, as Ben-Ner (1988) points out, an LMF can easily degrade into a KMF if the supply price for membership rights is less than the demand price tempting incumbent LMF owners to hire workers for a fixed wage. The keys to correcting an imperfect membership market are as multifarious as the reasons preventing the market from clearing in the first place and whether imperfect membership markets will prove fatal to the growth, through underinvestment, of the LMF depends on how competitive the market for LMF control can be made. If we take credit and insurance market imperfections as the primary factors keeping membership share prices below the market clearing rate, then any of the following policies could serve as possible solutions: direct extension of government credit to workers, or government guarantees to private lenders who finance worker membership fees, government income support for workers adversely affected by unforeseen shocks in the industry level, full disclosure of the risk level of incumbent LMFs through external monitoring, and the reliance on informal compensation packages when members depart like those found in Meade’s (1972) Inegalitarian Cooperative (Dow 1993, pg. 194). The impact of financing on the establishment of a market clearing rate for membership shares operates on both the supply side and demand side of the equation. On the supply side, the equilibrium membership price reflects the value of jointly owned assets (the price of membership being the difference between the present value of the LMF’s projected net worth and the market reservation wage) with a higher equity to debt ratio driving prices up. On the demand side, limited worker wealth in combination with credit rationing will cause prospective workers to undervalue the membership shares of the LMFs they wish to join. The main takeaway for our present investigation is that while a perfect market for membership rights as proposed by Dow and Sertel will solve the underinvestment problem present in LMFs* and PCs*, the establish of a competitive membership market, which is brought as close to theoretical market clearance as possible, depends on the resolution of our final financing problem: which method, non-voter equity, bonds, or quasi-equity shares, leads to the most optimal risk sharing agreement between risk-averse workers and risk-neutral creditors, and hence the most cost-effective solution to financing for the LMF. The answer to that question is beyond this scope of this paper however. 5. Conclusion Financing difficulties, in the form of costly access to external financing, were said to exist at the LMF formation stage and during the course of an LMFs lifespan in the form of underinvestment. These two respective financing problems, one entering at the firm’s birth and the other during a firm’s active life, are consistent with those general class of hypotheses which seek to account for the rarity of LMFs on the basis of the capital constraints facing workers who are poor and risk averse. I argued that this general class of capital constraint arguments provide the causal link from the qualitative asymmetry between capital and labor (capital is alienable while labor is inalienable) to the low emergence rate of LMFs. In the last section I hinted whether equity-like ‘risk participation bonds’ (McCain 1977) offering variable income obligations to bond holders can directly solve the start-up financing problems facing prospective worker-owners and indirectly solve, when combined with a market for membership rights, the underinvestment issues facing incumbent LMFs. If such a proposal were workable in practice it has the potential to undermine many of the arguments conceptually linking control rights to residual claimancy and asset ownership, hence providing a way of possible way to create a democratically controlled economy and challenge the intra-firm hierarchy of the neoliberal order. 6. Bibliography

|